Why Houston Homeowners Insurance Can Differ Block by Block

Two houses on the same Houston street can look almost identical and still have very different homeowners insurance. Same square footage, same year built, same style, yet one owner pays more and has different coverage options. That feels confusing until you know how local the risk really is.

Homeowners insurance in Houston is built on small details. Carriers look at your exact address, not just your ZIP code. A few houses closer to a bayou, a different drainage slope, or an older roof on your side of the block can all change how a policy is written. In this article, we will walk through the neighborhood-level details that often explain why one home pays less or has different coverage than another right next door.

How Micro-Location Shapes Your Homeowners Rates

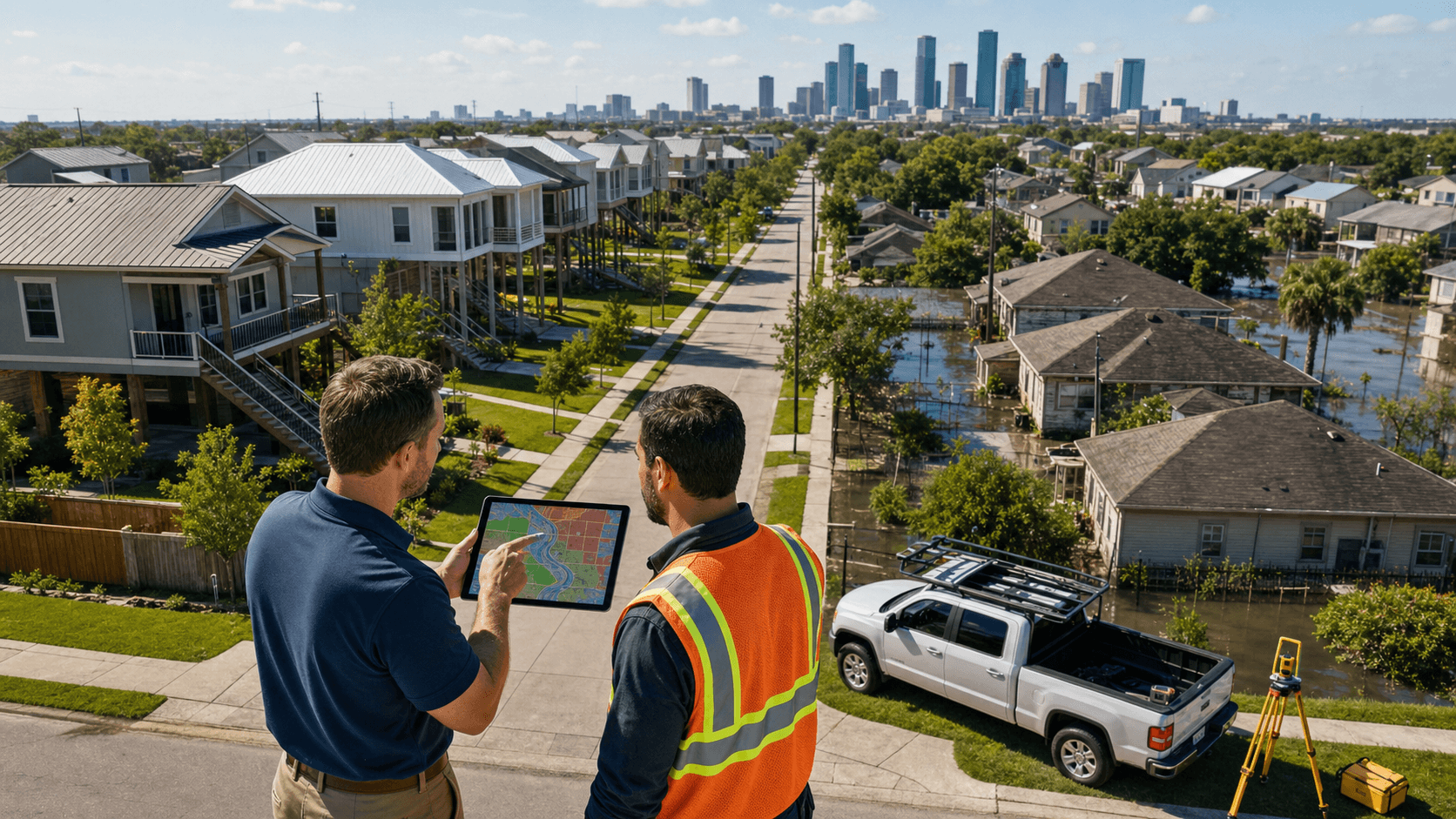

In Houston, water is one of the biggest concerns. Your distance from floodplains and bayous, like Buffalo Bayou, Brays Bayou, and White Oak Bayou, matters a lot. Carriers study maps that show exactly how water is expected to move when heavy rain hits. Sometimes a home is just far enough from a mapped area to be rated differently than a neighbor only a short walk away.

A small change in elevation can also make a difference. Homes that sit slightly lower on a street, or closer to a dip in the road, may be seen as more likely to collect water. That can affect:

- Whether flood coverage is strongly recommended

- What kind of deductibles a carrier offers

- How comfortable a carrier feels writing a policy at all

Fire protection scores also play a part. These scores can change from one block to the next, even inside the same ZIP code. Carriers look at:

- How close your home is to a staffed fire station

- Whether you have easy access to working fire hydrants

- The type of municipal services that serve your area

On top of that, construction details are not always the same on every street. One block might have newer roofs, updated electrical systems, or different foundation types than the block behind it. Carriers may price your policy based on:

- Age and condition of the roof

- Type of roofing materials

- Type of foundation and any known issues

- Whether plumbing and electrical have been updated

These are all very local details, and they help explain why two similar homes can end up with very different rates and coverage options.

Flooding, Drainage, and Houston's Summer Storm Season

Early summer in Houston means it is time to think about hurricane season and heavy rain. This is when many homeowners start to worry about how their coverage would respond if a tropical system sits over the city and drops inches of rain in a short time.

Drainage patterns are one of the biggest reasons risk can change on opposite sides of the same street. For example, one side of the road might have:

- Higher curb-and-gutter systems

- Better storm drains and inlets

- Slightly higher street elevation

The other side might rely on open ditches or have fewer drains, so water stays longer. Carriers look at these patterns when they model flood and water risk.

It is also important to know what standard homeowners insurance usually covers and what it does not. In general, typical homeowners policies often handle:

- Wind damage from strong storms

- Hail damage to roofs and siding

- Some damage from falling trees or debris

However, rising water from outside, like street flooding, bayou overflow, or water that seeps in from heavy rain, is usually not covered under a standard homeowners policy. That type of damage is often considered a flood issue, which is why separate flood insurance may be strongly recommended on some blocks, even if a lender does not require it.

Crime, Claims History, and Your Exact Address

Risk is not only about water and wind. Local crime patterns can shape homeowners insurance as well. Two subdivisions that share a main road can have very different crime levels inside their gates or at their entrances. Some areas see more:

- Burglary and break-ins

- Theft from garages, sheds, or vehicles

- Vandalism or property damage

Carriers often review detailed crime data by area, which can change how they view the risk of theft-related claims at your address.

Claims history also follows a property. If your home has had several claims in the past, even before you bought it, some carriers may be more careful about how they price or structure a policy. In some cases, a pattern of claims in a small area can make carriers more cautious in that neighborhood.

The good news is that security upgrades can help. Things like:

- Monitored alarm systems

- Cameras and smart doorbells

- Motion lighting and good exterior lighting

- Active neighborhood watch programs

can show carriers that the risk of theft or damage is being taken seriously. Sometimes, these steps can also open doors to better options, depending on the carrier and the rest of your situation.

HOA Rules, Renovations, and Hidden Coverage Gaps

Two subdivisions separated by a fence can have very different HOA rules. Those rules affect what your home looks like, and that can change what it would cost to rebuild. Some HOAs might require:

- Specific roofing materials or colors

- Certain types of siding, brick, or stone

- Approved fencing styles and heights

If your HOA includes community pools, parks, or other shared spaces, there can also be unique liability concerns in your area that carriers consider.

Inside the home, renovations often vary from house to house. On one block you might see:

- Converted garages or added living spaces

- Backyard structures like pergolas, sheds, or outdoor kitchens

- Upgraded kitchens and bathrooms with higher-end finishes

These changes can increase the cost to rebuild your specific home, but the policy is not always updated to match. That is where hidden coverage gaps can appear. It is important to look at:

- Dwelling limits, to see if they still match today's rebuild costs

- Extended replacement cost options, which can offer a buffer

- Endorsements for special features or added structures

When coverage does not keep up with your home and your HOA rules, you may have surprises at claim time, even if your neighbor with a very different setup is fully protected.

Smart Steps Houston Homeowners Can Take Today

Since risk is so local, the best starting point is a block-by-block review of your homeowners insurance before peak hurricane season. This is less about chasing the lowest price and more about comparing:

- Coverage types and limits

- Deductibles for wind, hail, and named storms

- How your policy treats water, flooding, and sewer or drain issues

A few practical actions can help you get a clearer picture of your home's risk and needs:

- Get an elevation certificate if you are in or near a flood-prone area

- Document recent upgrades with photos and receipts

- Review your roof age and condition

- Improve home security where it makes sense

- Ask targeted questions about flood insurance, wind coverage, and extended replacement cost tied to your exact address

About Ricky Wong and the Navigant Insurance Team: Navigant Insurance is a Houston-based independent insurance agency dedicated to protecting Texas families and businesses with thoughtful, customized coverage. Led by Ricky Wong and supported by the broader Navigant team, the agency draws on two decades of experience to understand each client's unique risks, explain options in clear language, and build long-term strategies that adjust as homes, families, and neighborhoods change from block to block.

Protect Your Houston Home With Coverage That Fits Your Life

Your home deserves protection tailored to Houston's unique risks, from Gulf Coast storms to everyday surprises. At Navigant Insurance, we take the time to understand your needs so we can match you with the right homeowners insurance in Houston. If you are ready to review your coverage or start a new policy, we are here to help. Have questions or want a personalized quote today? Just contact us.